{kind=link}

[ad_1]

Regardless of an extended record of issues that Constancy’s retirement planning instrument doesn’t do, I nonetheless use it as a high-level mannequin. The planning train I did on the finish of final yr revealed two elementary drivers of monetary success in retirement.

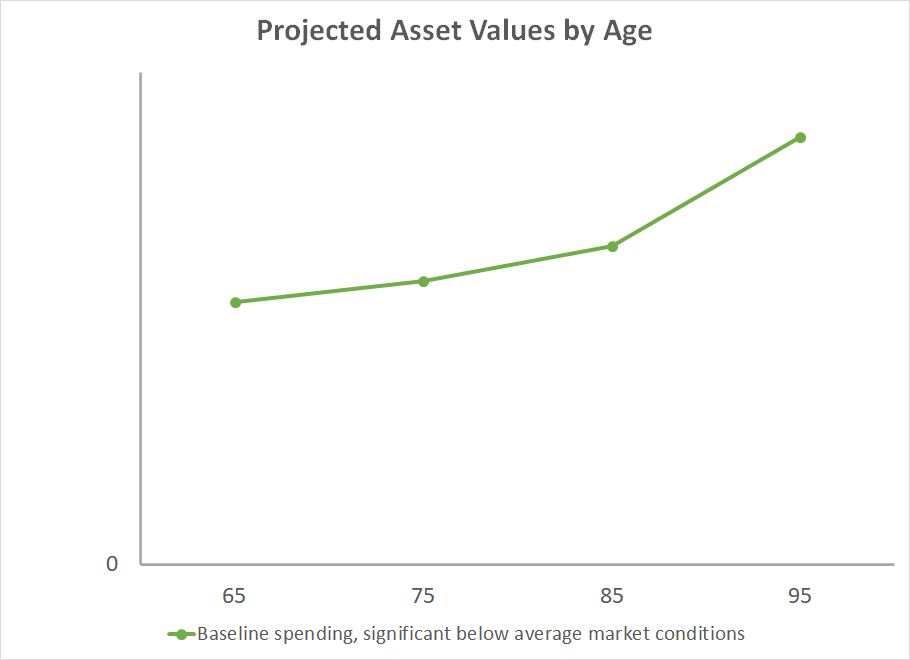

Baseline Spending

First, I created a baseline annual spending. The planning instrument confirmed a desk of the projected values of our investments at totally different ages when the funding returns are “considerably under common.” Considerably under common means “a situation wherein your final result was profitable 90% of the time” utilizing historic knowledge. I created this chart by sampling a couple of age milestones from the desk:

All values are in right now’s {dollars}. I’m not displaying numbers on the vertical axis for apparent causes.

Our funding portfolio is projected to extend whereas we take withdrawals to assist the deliberate annual spending. That’s each good and dangerous. It’s good as a result of it reveals we have now sufficient for our retirement. It’s dangerous as a result of we don’t want or need 60% more cash at age 95 than at age 65.

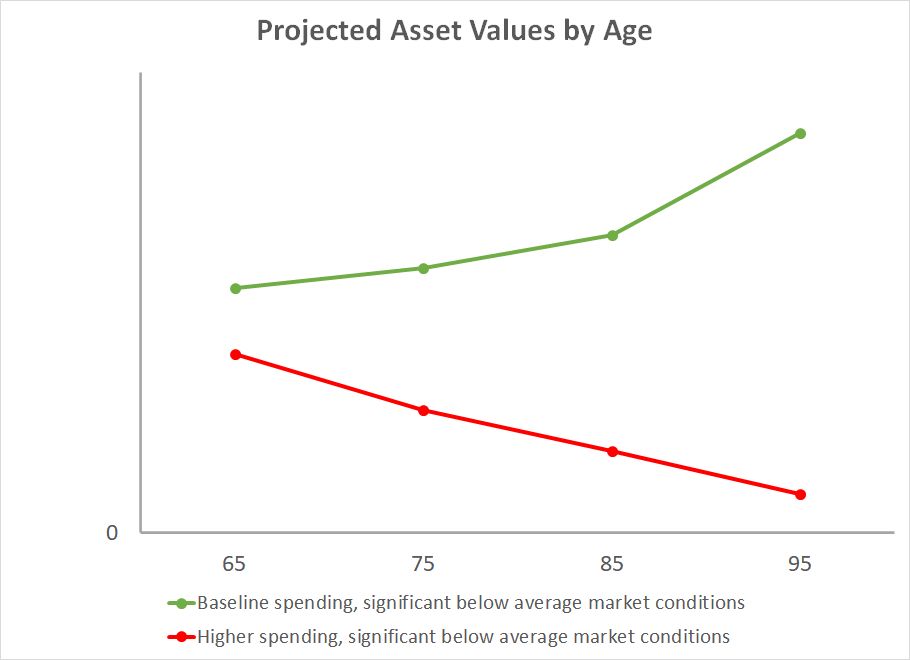

Larger Spending

Subsequent, I elevated the annual spending by 20%. The planning instrument confirmed a distinct set of projected values:

Now the projected values go down with age. It will get dangerously near zero at age 95. Which means our sustainable spending is someplace between these two ranges. If the longer term market returns are under 90% of returns up to now, we are able to nonetheless spend just a little greater than the baseline plan however not 20% extra.

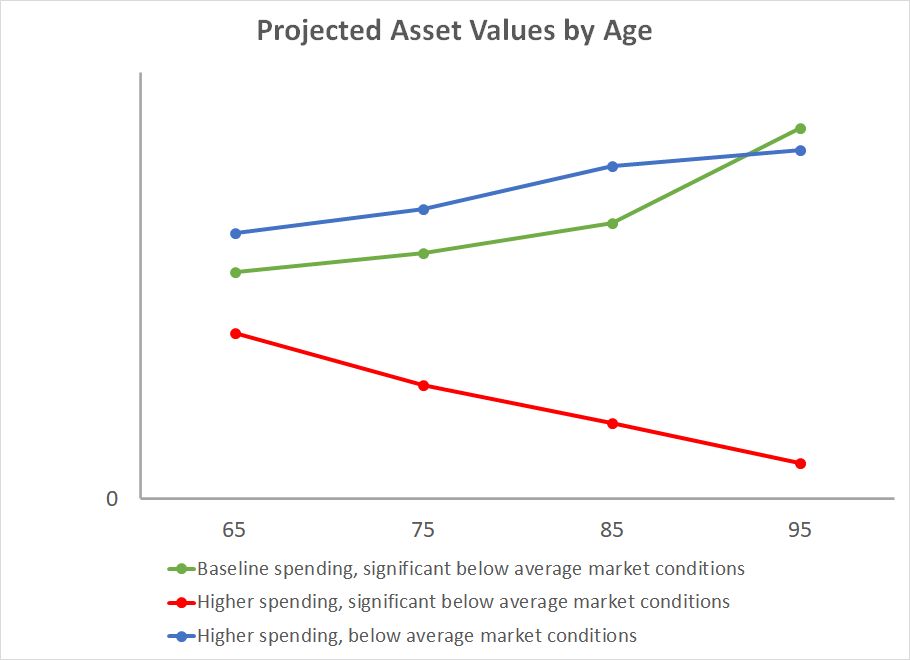

Higher Market Circumstances

The planning instrument additionally produced a desk of projected values for returns merely under common however not considerably under common. Under common means “a situation wherein your final result was profitable 75% of the time” versus 90%. The projected asset values beneath these higher market circumstances whereas supporting the upper spending seems just like the blue line on this chart:

It reveals that if the returns are solely under common — not considerably under common — our property could be increased than the baseline situation by means of age 90 whereas supporting 20% increased spending yearly.

Elementary Drivers

After I offered these three eventualities to my spouse, she identified that it was solely too apparent.

“You didn’t need to run a elaborate instrument to inform me that increased spending will drain our investments sooner and higher returns will assist.”

She advised me the identical factor after I mentioned I found the secrets and techniques to a fats 401k 11 years in the past.

It’s apparent as a result of it’s true. Spending and funding returns are certainly the 2 elementary drivers of monetary success in retirement as a result of they compound. We will deal with low returns (the inexperienced line) or increased spending (the blue line) however not each yr after yr if we dwell lengthy (the pink line).

Once we consider the same old consternations in retirement planning — when to assert Social Safety, which accounts to withdraw from first, when and the way a lot to transform to Roth, buckets technique or proportional withdrawals, purchase an annuity or not, … — every little thing added collectively can’t alter our retirement trajectory as a lot as our annual spending and funding returns.

If we’re on the pink line as a result of our annual spending is simply too excessive relative to the funding returns, essentially the most optimum techniques in Social Safety claiming, Roth conversion, and withdrawal sequencing gained’t yank us again to the inexperienced line. We’ll want to cut back spending. If we’re on the blue line as a result of we aren’t so unfortunate with funding returns, we’ll just do positive even when we aren’t so intelligent in retirement planning techniques.

You don’t have to make use of Constancy’s retirement planning instrument to see this impact. Some other instrument will present the identical two elementary drivers.

Make It Sturdy

Retirement planning techniques are helpful however we should always make our plan NOT depend on them. If optimum executions of Social Safety claiming, Roth conversion, and withdrawal sequencing make or break our retirement, it means our plan is too fragile. It isn’t sturdy sufficient when a slip in execution, a miscalculation, or a change of legal guidelines will knock us off observe.

The aim ought to be to make our retirement profitable regardless. Once we get our spending proper for the market circumstances, any optimization techniques will solely be icing on the cake, and suboptimal executions gained’t jeopardize our retirement. If we get our spending unsuitable for the market circumstances, no quantity of optimization will rescue our retirement.

***

We’ll be watching the trajectory of our investments. If we see we’re vulnerable to happening the pink line when we have now a mixture of excessive spending and low returns, we’ll cut back spending and attempt to transfer towards the inexperienced line. If we see that the market returns aren’t too dangerous, we’ll know we have now extra leeway in our spending. That’s how we’ll hold our eyes on the 2 elementary drivers of monetary success in retirement.

I advised my spouse that’s all she must do if one thing occurs to me. The whole lot else is optionally available. How does SECURE Act 2.0 alter the monetary success of our retirement? It doesn’t, as a result of it doesn’t change the 2 elementary drivers.

Say No To Administration Charges

In case you are paying an advisor a proportion of your property, you might be paying 5-10x an excessive amount of. Learn to discover an unbiased advisor, pay for recommendation, and solely the recommendation.

[ad_2]